CBR INTELLIGENCE NOTE

CBR Intelligence Note | Vol. 1, No. 11

Joseph Cox

Managing Partner, Joseph Cox & Associates Limited

Publisher, Caribbean Business Review

May 5, 2026

Classification: Public

Abstract

The liquidation of Spirit Airlines reflects the interaction of three forces: geopolitical energy shocks, fragile ultra-low-cost carrier economics, and an increasingly concentrated airline industry. While the immediate trigger was a sharp escalation in fuel costs, the more consequential outcome lies in the post-exit shift from competitive pricing discipline to pricing power. This shift is amplified in the Caribbean, where structural constraints and weakening regional carriers limit substitution effects. The result is a two-speed regional impact—manageable in larger markets, but potentially destabilizing in smaller, highly dependent economies.

Key Judgements

Energy shocks act as accelerants, not root causes, of corporate failure

Ultra-low-cost models deliver affordability but exhibit extreme fragility under volatility

The removal of low-cost carriers enables a rapid reversion to pricing power

Industry concentration (≈80% controlled by four U.S. carriers) amplifies this effect

The Caribbean faces asymmetric impacts, from fare escalation to demand destruction

Regional aviation weakness is shifting the Caribbean from exposure to dependency

Introduction

Spirit Airlines once played a critical role in democratizing air travel, particularly for price-sensitive consumers and diaspora communities. The carrier, the ninth-largest in the US, operated more than 700 Caribbean-bound departures in August 2025 alone, underscoring its importance to regional airlift. Its collapse on May 2, 2026 is being widely framed as a casualty of rising fuel costs—another airline undone by volatility in global energy markets. That explanation is not wrong. But it is incomplete.

Nonetheless, a roughly 70% increase in fuel prices—pushing costs from near $2.24 toward $4.00—translated into a $360 million shock that the airline could not absorb. For an ultra-low-cost carrier like Spirit Airlines, where fuel typically accounts for 20–30% of operating costs, such a spike is existential.

However, what has occurred is not simply a corporate failure. It is a signal of how fragile business models, geopolitical shocks, and market structure intersect—and amplify one another.

For more than a decade, Spirit Airlines shaped airfare dynamics across the United States and the Caribbean, not through scale, but through pricing discipline. Its ultra-low-cost model—built on high aircraft utilisation, aggressive fare compression, and ancillary revenue—expanded access to travel, but left little margin for volatility.

When geopolitical tensions—particularly around critical transit routes such as the Strait of Hormuz—pushed fuel costs sharply higher, that model did not adjust. It failed.

The more important consequence, however, emerges after the collapse.

Spirit’s presence exerted a measurable disciplining effect on fares, particularly on leisure-heavy routes linking the Caribbean to major U.S. gateways. Its exit removes that constraint. In its absence, airlines are no longer forced to price defensively; they are able to optimise for yield.

Its disappearance therefore creates a vacuum that extends well beyond its market share.

The critical question is not whether other airlines can replace the seats. In many cases, they can. The question is whether they will replace the pricing.

This Intelligence Note argues that Spirit’s collapse marks a transition from a regime of price competition to one of pricing power, with effects that are neither uniform nor temporary. Instead, they will be shaped by market depth, structural constraints, and the Caribbean’s growing dependence on external carriers.

Anatomy of War: From Price Movement to Risk Repricing

The immediate catalyst for the collapse was a sharp escalation in fuel costs. However, within that context the United States–Israel–Iran conflict is not simply moving energy prices. It is re-pricing risk across the global economy, altering how costs are transmitted, absorbed, and ultimately borne.

This repricing unfolds along three interconnected channels.

First, it exerts pressure on firms through cost pass-through. As input costs rise—particularly energy and transport—businesses face a narrowing set of choices. They can absorb the increase, compress already thin margins, or pass it on to consumers, weakening demand. In either case, the adjustment is immediate and consequential.

Second, it exposes fragility. Firms operating with high leverage, limited pricing power, or structurally thin margins are unable to absorb sustained cost increases. These entities do not adjust gradually; they fail abruptly. In this sense, the shock does not create weakness—it reveals it, and accelerates its outcome.

Third, the adjustment transmits directly to households. Higher fuel and transport costs feed into airfares, food prices through logistics, and electricity costs. What begins as a geopolitical event is therefore converted into a broad-based increase in the cost of living.

But the deeper story is structural.

Certain business models are not designed to operate under conditions of volatility. Ultra-low-cost carriers are among the most exposed. Their economics depend on stable fuel prices, consistently high load factors, and the ability to generate ancillary revenue from a price-sensitive customer base. These conditions are sustainable in a stable cost environment. They are not resilient in a volatile one.

When fuel prices spike—particularly amid geopolitical disruptions affecting critical transit routes such as the Strait of Hormuz—the model does not compress. It becomes non-viable.

The implication is critical.

Geopolitical energy shocks do not simply raise costs. They invalidate business models built on stability assumptions, accelerating collapse and redistributing losses away from firms and toward consumers.

But the relevance of the energy shock lies less in its origin than in its function.

It acted as a stress test.

Airlines with diversified revenue streams, scale advantages, and stronger balance sheets were able to absorb or pass through the increase. Those without such buffers were not. Spirit fell into the latter category—not because it was uniquely exposed to fuel, but because its model left no room for volatility.

The shock did not create weakness. It revealed it.

The Model: Affordability Built on Fragility

Spirit’s ultra-low-cost model was built on precision. Aircraft were kept in the air for as many hours as possible. Routes were designed to avoid costly hub structures. Services were stripped down and unbundled, allowing passengers to pay only for what they used. The result was a pricing structure that opened travel to segments of the market that traditional carriers could not profitably serve.

But this efficiency came at a cost.

The model depended on stability—particularly in input costs. There was little margin to absorb unexpected increases, and limited ability to raise fares without undermining the very demand it was designed to capture.

When fuel prices rose beyond a certain threshold, the model did not bend. It broke.

This is the central paradox of the ultra-low-cost carrier: it expands access in normal conditions, but becomes structurally fragile in abnormal ones. And when it fails, the consequences extend beyond the firm itself, because the discipline it imposed on the market disappears with it.

Market Structure: Concentration and Asymmetry

The consequences of Spirit’s exit cannot be understood without reference to the structure of the industry into which it exits.

The U.S. airline market is highly concentrated, dominated by United Airlines, American Airlines, Delta Air Lines, and Southwest Airlines, which together control nearly 80% of available capacity. This concentration is the product of successive waves of consolidation, which have reduced the number of competitors while increasing scale and network power.

In such a system, asymmetry defines outcomes.

This asymmetry operates through three reinforcing advantages:

Scale and network depth — large carriers optimise across integrated route systems

Financial resilience — diversified revenue streams absorb cost shocks

Pricing flexibility — control over capacity and frequency enables yield optimisation

Smaller carriers, by contrast, operate with limited buffers and transmit shocks through failure.

The exit of a smaller player therefore has effects that are disproportionate to its size. Competition in aviation is not simply a function of how many seats are available, but how those seats are priced.

In many markets, Spirit’s capacity will be replaced. Aircraft will be redeployed, frequencies increased, and displaced passengers absorbed. From a purely quantitative perspective, capacity may appear largely intact and that the system has adjusted.

But discipline does not.

Spirit’s presence anchored the lower bound of pricing. Without that anchor, pricing behaviour shifts. Discounts narrow, pricing algorithms adjust upward, and fares begin to reflect demand tolerance rather than competitive pressure.

What emerges is not price gouging in the legal sense, but something more fundamental:

Pricing begins to reflect what the market can bear, rather than what competition forces it to accept.

This is not collusion. It is structure.

And its outcome is predictable: a shift from price competition to yield optimisation, with higher average fares and reduced access for the most price-sensitive segments.

The Timing: A Shock Amplified

The timing of Spirit’s collapse compounds its impact.

The airline ceased operations just as the peak summer travel season begins—a period characterized by rising demand, high load factors, diminution of low-cost inventory and increased reliance on discretionary travel. At precisely the moment when demand is strongest, the supply of low-cost seats has been reduced.

The immediate result is not subtle. Last-minute fares rise sharply, particularly on routes that were heavily dependent on budget carriers. For price-sensitive travellers, the effect is immediate and binding.

This is not a gradual adjustment to a new equilibrium. It is a front-loaded repricing of the market.

The Caribbean: Fragility Before the Shock

Nowhere are these dynamics more consequential than in the Caribbean.

The Region’s aviation system was already constrained prior to Spirit’s collapse. High operating costs, layered taxes and fees, fragmented regulatory frameworks, and thin route density have long limited connectivity. On many routes, taxes and charges account for 30–50% of total ticket prices, making short-haul travel disproportionately expensive.

These constraints are structural:

High tax and fee burdens embedded in ticket pricing

Thin route density, limiting competition and frequency

Undercapitalised regional carriers with limited scale

Fragmented policy frameworks across jurisdictions

At the same time, regional carriers have struggled to achieve competitiveness. The result is a system that relies heavily on external airlines to provide connectivity, particularly to major tourism markets in North America.

Spirit’s role within this system was therefore outsized. It did not dominate capacity, but it shaped pricing dynamics across key corridors. Its presence-imposed discipline. Its exit removes it.

Substitution Without Competition: The Jamaica Case

In larger markets such as Jamaica, the immediate effects are likely to be contained. According to Jamaican Tourism Minister Edmund Bartlett, Spirit accounted for less than 3% of passenger traffic, and routes such as Fort Lauderdale are well served by multiple carriers. Substitution is therefore feasible in the short term.

But substitution preserves capacity—not competition.

Other airlines are expected to absorb demand, but they are unlikely to replicate the pricing. Over time, fares will adjust upward, reflecting the absence of a low-cost anchor. The impact is therefore not one of disruption, but of repricing.

Where the Shock Bites: Thin Markets and Structural Exposure

The picture changes dramatically in smaller markets.

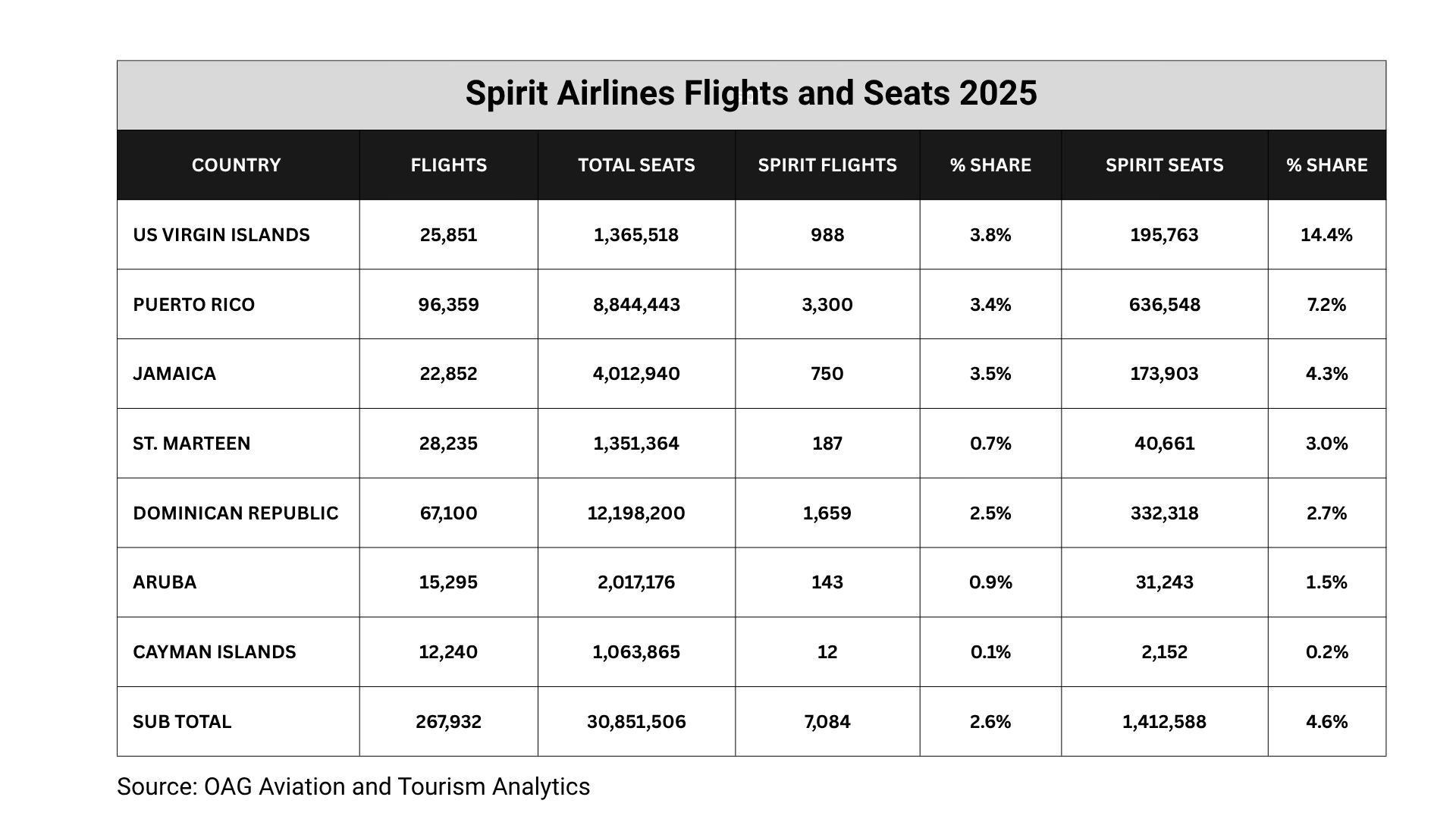

In the United States Virgin Islands, Spirit accounted for ~14.4% of total seat capacity— compared with approximately 4.3% in Jamaica and 7.2% in Puerto Rico. Here, the loss of a single carrier cannot be easily absorbed. Capacity gaps emerge, fares rise more sharply, and the elasticity of demand becomes a binding constraint.

In such markets, the loss of a carrier is not replaced. It is felt.

The consequences extend beyond aviation. Tourism flows weaken as travel becomes less affordable. Short-term rental markets—heavily dependent on budget travellers—are particularly exposed. These travellers do not simply switch to cheaper accommodation when airfares rise. They change destinations altogether.

The result is not a redistribution of demand, but its contraction.

Spirit served only seven Caribbean destinations, but its importance varied dramatically.

Analytical Signal: Aviation Dependency

The uneven impact of Spirit Airlines’s exit reflects a deeper structural reality—Caribbean markets are not equally positioned to absorb shocks in airlift or pricing.

A simple comparative lens highlights three tiers of exposure:

High Exposure — United States Virgin Islands

A heavy reliance on a single low-cost carrier—previously accounting for 14.4% of total seat capacity—means both capacity and pricing are affected simultaneously.Elevated Exposure — Puerto Rico and OECS markets

Greater route coverage exists, but limited carrier diversity and thin route depth constrain competitive responses, increasing susceptibility to fare escalation.Moderate Exposure — Jamaica

With Spirit accounting for less than 3% of passenger traffic (approximately 30,000–40,000 summer seats), substitution is feasible—but pricing discipline weakens.

The distinction is critical.

The issue is not whether capacity can be replaced—but how pricing behaves once it is.

This provides an early framework for understanding aviation dependency as a macroeconomic risk, with smaller markets facing both capacity and demand shocks, while larger markets experience primarily a repricing of access.

Tourism Transmission: From Fare Increases to Demand Destruction

The impact of Spirit Airlines’s exit is not evenly distributed across the tourism ecosystem. It is concentrated in one segment—the price-sensitive leisure traveller—that has quietly underpinned a significant share of Caribbean travel demand.

This segment is defined by three characteristics:

high price sensitivity, with travel decisions anchored to total trip cost

leisure-driven demand, often discretionary rather than essential

alignment with short-term rentals, including Airbnb and similar platforms

In several Caribbean markets, this cohort accounts for an estimated 30–40% of total accommodation demand. Its importance lies not just in volume, but in its marginal role—these are the travellers who expand the market when prices fall.

That dynamic now reverses.

When airfares rise, this segment does not behave like traditional hotel-based travellers. It does not trade down to cheaper accommodation or compress spending elsewhere. Instead, it exits.

Trips are postponed. Destinations are substituted. In some cases, travel does not occur at all.

This is the critical distinction:

Higher airfares do not reallocate demand within the system—they remove it from the system.

The consequence is not simply higher prices, but a contraction in effective demand. Short-term rental operators—whose business models are closely tied to this segment—are therefore disproportionately exposed. Unlike large hotel chains, they lack the buffers of brand loyalty, corporate travel, and premium segments that are less sensitive to price increases.

The result is a two-tier tourism impact:

Hotels experience margin pressure but retain demand

Short-term rentals face demand erosion as travellers exit entirely

In this sense, the loss of a low-cost carrier does more than raise fares—it reshapes the composition of demand, shifting the market toward higher-income travellers while excluding those at the margin.

Market Signal: Pricing Power and Demand Trade-Offs

Financial markets reacted immediately to Spirit’s collapse, with JetBlue Airways rising by 7.4% and Frontier Airlines by 8.8%.

These movements are not incidental. They reflect a forward-looking expectation that the removal of a low-cost competitor will:

allow for higher average fares

support margin expansion

reduce competitive pricing pressure

However, this optimism embeds an important assumption—that demand will remain sufficiently resilient to absorb higher prices.

The analysis above suggests that this assumption may only partially hold.

While higher-income and less price-sensitive travellers will continue to fly, the loss of the budget segment introduces a structural trade-off:

Pricing power increases—but the addressable market contracts.

This creates a more complex equilibrium. Airlines may achieve stronger yields, but at the cost of reduced volume in certain segments and destinations. For smaller Caribbean markets, where demand is already thin, this trade-off is particularly consequential.

A Deeper Constraint: The Erosion of Regional Capacity

Compounding this vulnerability is the weakness of the region’s own carriers. The withdrawal of Caribbean Airlines from key routes, despite strong underlying demand, illustrates the problem.

The airline ended all service between Jamaica and Fort Lauderdale effective November 2, effectively severing direct links between Kingston, Montego Bay, and South Florida.

The issue was not demand—it was performance.

In May 2025, Caribbean Airlines offered nearly 6,000 seats on the Kingston–Fort Lauderdale route. Only 1,892 passengers travelled, implying a 32% load factor. Montego Bay performed only marginally better, with utilisation in the 39–40% range.

By contrast, competing carriers were operating at significantly higher capacity utilisation. JetBlue Airways and Spirit Airlines filled between 75% and 88% of their seats—even as Spirit operated under bankruptcy protection—while Southwest Airlines exceeded 80% utilisation.

The disparity is instructive.

This is not a demand constraint—it is a competitiveness constraint.

Operational inefficiencies, network positioning, pricing strategy, and customer alignment all appear to have limited the regional carrier’s ability to compete effectively on high-traffic routes.

This matters because regional carriers could, in principle, provide a counterweight to external pricing power. In practice, their ability to do so is constrained.

The Caribbean is therefore not only exposed to external shocks—it is increasingly dependent on external responses.

Transmission Chain: From Shock to Systemic Cost

The dynamics set in motion by the collapse of Spirit Airlines are best understood not as a single event, but as a cascading transmission process.

What begins as a geopolitical shock propagates through the aviation system and ultimately into the real economy:

Energy Shock → Cost Surge → Carrier Failure → Loss of Pricing Discipline → Pricing Power → Asymmetric Impact → Economic Cost

Each stage reinforces the next.

Rising fuel costs compress margins, exposing fragile business models. Carrier failure removes competitive constraints, allowing remaining firms to reprice. That repricing does not occur uniformly. It is shaped by market structure—absorbed in larger markets, but amplified in smaller, thinner ones.

The final adjustment is not contained within the aviation sector. It is transmitted outward:

Households through higher travel and cost-of-living pressures

Tourism-dependent sectors through reduced demand and occupancy

Small economies through weakened connectivity and competitiveness

In this sense, the airline collapse is not the endpoint of the shock. It is the mechanism through which the shock is redistributed across the system.

Strategic Implications: From Market Adjustment to Structural Risk

The implications extend beyond aviation. They reveal how the Caribbean economy is structured—and where its vulnerabilities lie.

Aviation as Economic Infrastructure

Air transport in the Caribbean is often treated as a commercial service. In reality, it functions as core economic infrastructure.

Tourism, trade, labour mobility, and diaspora connectivity all depend on reliable and affordable airlift. When pricing rises or connectivity weakens, the impact is not marginal—it is systemic. Growth slows, integration weakens, and economic activity becomes more concentrated.

In small island economies, airlift is not optional—it is foundational.

External Dependency and Pricing Control

The Spirit collapse underscores a deeper structural issue: the region’s reliance on external carriers to determine pricing and capacity.

As low-cost entrants exit and regional carriers weaken, pricing decisions increasingly shift outside the Caribbean. Airlines optimise for global network returns, not regional development objectives. Routes are added or removed based on yield, not connectivity needs.

The Region therefore loses influence over:

pricing structures

route frequency

market access

The Caribbean does not set the terms of its connectivity—it responds to them.

The Emerging Trade-Off: Yield vs Access

A final implication lies in the emerging trade-off between airline profitability and market accessibility.

With the removal of low-cost competition:

airlines gain pricing power

margins improve

yields rise

But this comes at a cost:

reduced participation by price-sensitive travellers

contraction in certain tourism segments

widening inequality in access to mobility

This is not simply a commercial adjustment. It is a structural shift in who the market serves.

Conclusion: From Exposure to Dependency

The collapse of Spirit Airlines does not produce a single outcome. It produces divergence.

In larger markets, capacity is replaced, but pricing discipline weakens. In smaller markets, capacity constraints and price increases combine to suppress demand. Across the Region, the balance of power shifts away from competition and toward concentration.

This is the deeper signal.

What disappears is not capacity—but constraint.

The Caribbean’s aviation system is moving from a position of vulnerability to one of dependency—where pricing, connectivity, and access are determined largely outside the Region.

What began as a fuel shock has evolved into a structural adjustment.

And the cost of that adjustment will not be borne by airlines alone. It will be absorbed by households, by tourism-dependent economies, and by a Region whose connectivity remains its lifeline.

Disclaimer

This document reflects the independent analysis and professional opinions of Caribbean Business Review.

It is provided for informational and discussion purposes only and does not constitute legal, financial, investment, or policy advice. While reasonable care has been taken, no representation is made as to completeness or accuracy.

© 2026 Caribbean Business Review. All rights reserved.

Advisory Note

For advisory engagements, strategic governance services and economic briefings, contact Joseph Cox & Associates Limited: enquiries@josephcox.org

Note: Selected CBR Intelligence Notes and extended analysis will be made available to subscribers as part of a premium tier in the near future.